The Tax Cuts and Jobs Act or “TCJA” of 2017 made multiple changes to the individual income tax, including changes limiting significantly the itemized deductions and increasing the standard deduction.

Itemized deductions are expenses allowed by the IRS that can decrease your taxable income. The standard deduction is a flat-dollar, no-questions-asked reduction in your taxable income. You can either take the standard deduction or itemize on your tax return. You can’t do both. The question is which method saves you more money by reducing the tax.

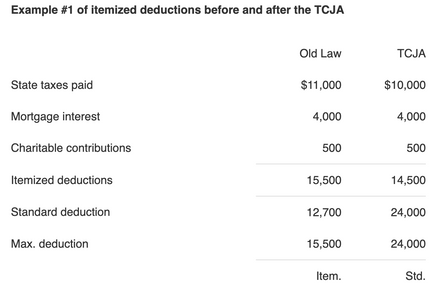

The standard deduction for married filing jointly increased from $12,700 to $24,000 from 2017 to 2018. The standard deduction for singles increased from $6,350 to 12,000 from 2017 to 2018.

The Tax Cut and Jobs Act (TCJA) changed materially the 1040 itemized deductions for 2018 in the following manner:

- Deduction for personal casualty and theft losses suspended (unless incurred in federally-declared disaster area);

- Limitations to the deduction for state and local taxes;

- Limitations to the deduction for home mortgage interest in certain cases;

- Eliminating most miscellaneous itemized deductions such as:

Deductions for employee business expenses;

Tax preparation fees;

Investment expenses, including investment management fees;

Employment related educational expenses;

Job search expenses;

Hobby losses;

Safe deposit box fees;

Investment expenses from pass-through entities;

Eliminates the limitation on itemized deductions for certain high-income taxpayers.

Limitations to the deduction for state and local taxes

If you itemize deductions on Schedule A, your total deduction for state and local income, sales and property taxes is limited to a combined, total deduction of $10,000 ($5,000 if married filing separately).

You have the option of claiming either state and local income taxes or state and local sales taxes (you can’t claim both). If you saved your receipts throughout the year, you can add up the total amount of sales taxes you actually paid; however, your deduction is limited to $10,000 ($5,000 if married filing separately) for a combined, total of state and local income, sales and property taxes.

Limitations to the deduction for home mortgage interest in certain cases

There are limitations on the deduction for home mortgage interest based in dollar limits of the mortgages you (or your spouse if married filing a joint return) took out after October 13, 1987, and prior to December 16, 2017, to buy, build, or substantially improve your home (called home acquisition debt), but only if throughout 2018 these mortgages plus any grandfathered debt totaled $1 million or less ($500,000 or less if married filing separately). Also, mortgages you (or your spouse if married filing a joint return) took out after December 15, 2017, to buy, build, or substantially improve your home (called home acquisition debt), but only if throughout 2018 these mortgages plus any grandfathered debt totaled $750,000 or less ($375,000 or less if married filing separately). These dollar limits apply to the combined mortgages on your main home and second home.You can also find debt defense attorneys as they can help you to overcome debt related issues.

The state and local tax (SALT) deduction has been one of the largest federal tax expenditures, with an estimated revenue cost of $100.9 billion in 2017. The estimated revenue cost for 2018 drops to $43.1 billion because the Tax Cut and Jobs Act (TCJA) significantly increased standard deduction amounts (thereby reducing the number of taxpayers who will itemize deductions) and capped the total SALT deduction at $10,000.

State and local taxes have been deductible since the inception of the federal income tax in 1913. Initially, all state and local taxes not directly tied to a benefit were deductible against federal taxable income. In 1964, deductible taxes were limited to state and local property (real and personal property), income, general sales, and motor fuels taxes.

Congress eliminated the deduction for taxes on motor fuels in 1978, and eliminated the deduction for general sales tax in 1986. It temporarily reinstated the sales tax deduction in 2004, allowing taxpayers to deduct either income taxes or sales taxes but not both. Subsequent legislation made that provision permanent starting in 2015. Starting in 2018, taxpayers cannot deduct more than $10,000 of total state and local taxes. That provision of the law is scheduled to expire after 2025.(1)